10 Reasons Why Long-Term Care Insurance Is Essential To Your Financial Plan

By Carmen I. Bississo, CIMA®, AIF®, CLTC, CAS®, CFS®

Long-term care insurance is designed to cover the cost of assistance with activities of daily living (such as dressing, eating, bathing, toileting, transferring/mobility, and continence) or additional support if you develop a cognitive disorder. This care is not covered by traditional health insurance and can become a huge financial burden if you don’t plan ahead.

Consider these ten key points as you evaluate if long-term care insurance is right for you.

1. You cannot count on the government or your health insurance to pay for your long-term care cost.

Medicare will only cover the full cost of custodial care for 20 days. Depending on your condition, it could pay for a maximum of 100 days. Beyond this, you are on your own.

The only government support available is through Medicaid, which essentially only provides funding when you run out of money. In most states, you cannot have more than $2,000 in assets under your name. Additionally, there are income and gifting limitations that apply and other considerations, depending on your family structure, age, and domicile.

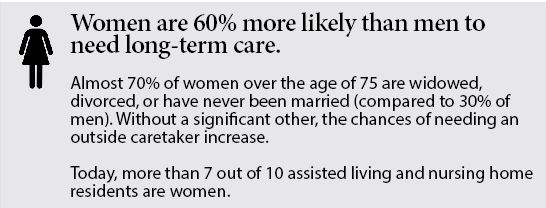

2. You have a high risk of needing long-term care in your lifetime, especially if you are a woman.

According to the U.S. Department of Health and Human Services, someone turning 65 today has almost a 70% chance of needing some type of long-term care assistance, and 1 in 5 will need it for longer than 5 years.

By 2050, the number of individuals using paid long-term care services in any setting (e.g., care at home, or residential care including assisted living or skilled nursing facilities) is expected to more than double from the 13 million in 2000 to 27 million people.

3. You cannot afford to wait!

It is important to act now while you are in good health as the cost for long-term care insurance is highly dependent on your physical condition. Many people believe that buying a policy later in life will help them save on premium costs. In reality, the longer you wait, the more expensive your options become, and the higher your risk of becoming uninsurable.

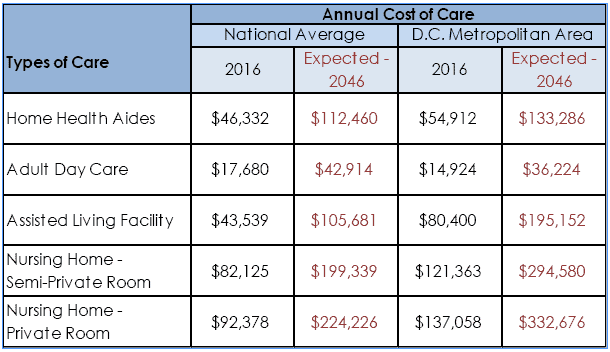

4. Costs of long-term care assistance will be much higher in the future—and where you live matters!

The good news about today’s medical advancements is that we will all live longer (though not necessarily healthier) lives. Unfortunately, longevity will increase our risk of needing long-term care services in the future, and we cannot predict what type of assistance we will have when the need for care arises.

The chart below demonstrates the annual costs of care for an individual today and the anticipated costs in 30 years. The chart compares the national averages with the DC/Metropolitan area.

Source: Genworth Cost of Care Study by CareScout, April 2016. Home Health Aides based on 44 hrs/week; Adult Day Care based on 5 days/week; Assisted Living Facility based on 12 months of care in private room, Nursing Homes based on 365 days of care)

For additional information on costs around the country, click here: Compare Long-Term Care Costs in the US

5. Don’t be a burden on your family.

Currently, 66% of home care in the U.S. is provided solely by family members, with children and grandchildren providing the majority of this care.

Three out of four of these caregivers work a paying job while simultaneously caring for their loved one. Often, they have to make accommodations such as cutting back hours or quitting altogether, which can have large financial implications on their future. Loss of earnings, Social Security benefits, job security, career mobility, health insurance and retirement savings are just a few examples of the sacrifices caregivers often have to make.

Every parent wants their child to feel safe and protected, not burdened by the financial and time constraints that come with caring for an aging loved one. Long-term care insurance can be part of the solution.

6. You choose where you want to receive care. You do not have to leave your home.

When was the last time you heard someone say: “I can’t wait to go to a nursing home!”? Without the proper insurance planning, you may not have a choice. Nursing homes are typically the only solution that is covered by Medicaid.

Today, long-term care insurance policies provide coverage irrespective of where you receive care – at home, in an adult day care, assisted living facility, nursing home or even in hospice care. Many current policies also add an alternative plan of care in the event that new forms of care become available in the future.

7. Reduce your risk of depleting your assets.

While many affluent investors can afford to self-insure, transferring the risk to the insurance company and preserving assets for future generations is a stronger long-term investment strategy.

8. You secure your access to the right type of care for your needs.

In the future, it will not be surprising to see assisted living and nursing home facilities accepting only those who can afford care.

As of 2013, there were more than 44.7 million Americans over the age of 65. By 2060, this age group will more than double in size.3 Given this, there will be an increasing demand for long-term care facilities and we will see longer waitlists and higher costs in the long run. Long-term care insurance can provide adequate funding to secure the care you need and where you need it.

9. Save on taxes.

There are several tax incentives used by state and federal governments to encourage the purchase of long-term care insurance. Many states offer tax credits and deductions. Federal tax incentives include allowing the use of health savings accounts (HSAs) to pay long-term care premiums, a tax deduction for premiums paid by employers or self-employed individuals, and a tax deduction for long-term care expenses equating to over 10% of your income. Please consult with your tax advisor for additional information.

10. Help gain peace-of-mind.

A long-term care insurance policy makes it easy for you to access the best type of care, and it can help to give your family peace-of-mind and the ability to focus on your well-being. In our experience, when there is no long-term care policy to rely on, the plan of care chosen is typically the most inexpensive which may not provide you with the level of care that you need. Often, the healthy spouse has concerns of running out of money and there may be a need or desire to protect assets for future generations.

You have options. Long-term care policies come in all shapes and sizes and your financial advisor can help you identify the one that is right for you. There are also ways to access long-term care protection with a life insurance or annuity product, also known as hybrid policies, which may better fit your needs than a stand-alone long-term care policy.

Irrespective of how you decide to protect yourself and your family for the possible need of long-term care assistance in the future, it is important that you have a plan in place and ensure that those close to you are informed. ■

To learn more about long-term care planning and steps you can take now to protect yourself, contact your financial advisor or

Related Posts